Economic & Market Overview

Equity and Fixed Income Markets have rebounded to a strong level YTD with the S&P 500 increasing 9.62% YTD and the Aggregate Bond Market jumping 4.91%. Both very solid returns after a wonderful return years in 2023 and 2024. These returns have moved long standing accounts well ahead of most planning objectives. *Data provided by Y-Charts as of 8/14/2025

Over the past quarter, markets have grown increasingly desensitized to the daily noise of political rhetoric and are instead focusing on real-time economic data. Concerns over extreme, long-term tariffs have eased somewhat, as the likelihood of more balanced trade agreements has increased.

Recent CPI and GDP readings, along with other key indicators, are painting a clearer picture: inflation is continuing to moderate (not great but not terrible), and the economy is slowing but certainly showing signs of resiliency. This mixed combination has strengthened market expectations for more accommodative monetary policy, including multiple interest rate cuts and potentially a renewed push for liquidity support and quantitative easing. Markets like the sweet spot of slowing enough to spark cheaper money and increased liquidity without slowing too much to create negative economic pressures like a recession. Remaining in this sweet spot allows companies to manage conditions and continue to drive increasing profit growth.

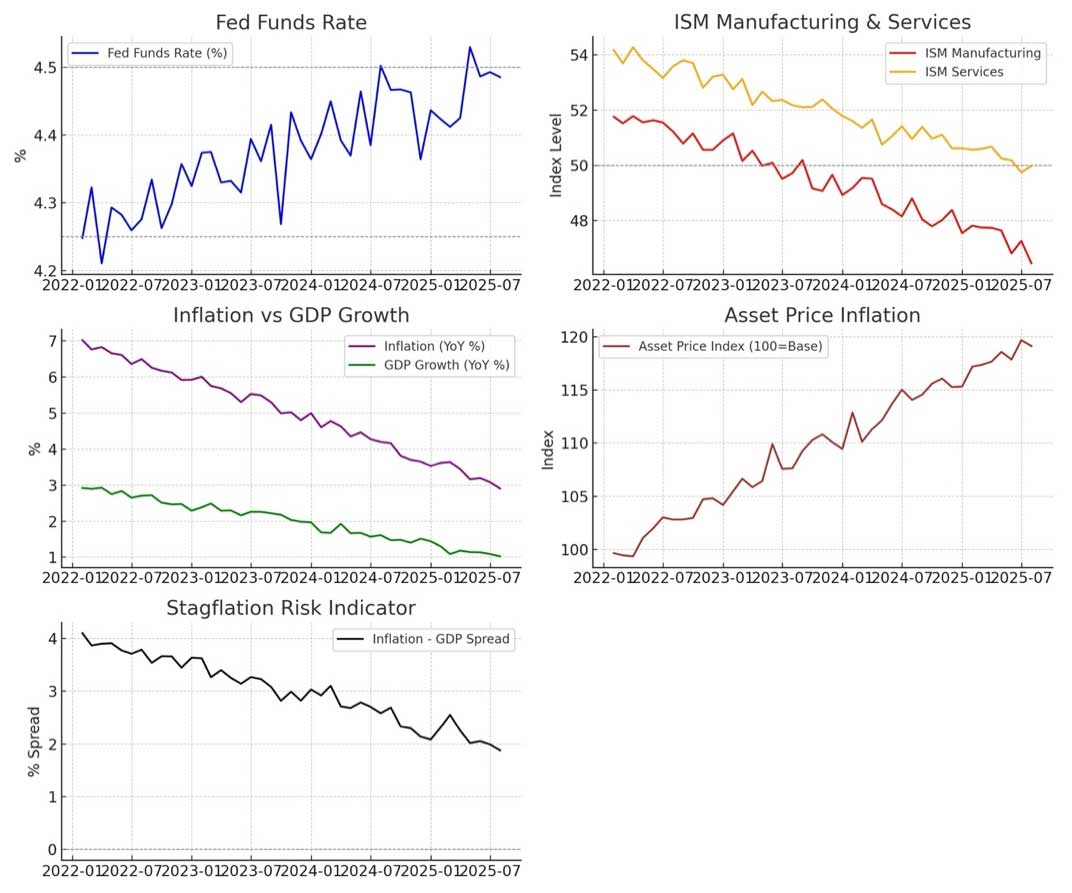

The FOMC met on July 29–30 and voted to keep the federal funds target range at 4.25–4.50%, marking the fifth consecutive pause in rate adjustments. While the Fed has not yet cut rates in 2025, the trajectory of recent data suggests that two 25 bp cuts—and possibly a third—may be on the table if disinflation and economic softness persist. Labor market conditions are easing, ISM Manufacturing remains in contraction territory (below 50), and the ISM Services Index for July barely held above the contraction line at 50.1. These readings point to a cooling economy where rate cuts may indeed be warranted.

However, we remain cautious. Parts of inflation remain very sticky and while we don’t believe tarrifs are long term inflationary, they can increase price pressures short term (more on that below). This increases the risk of continued stagflation—a cycle in which inflation continues to outpace GDP growth. We are not convinced rate cuts alone will be the catalyst for propelling the economy forward. Historically, it is economic growth (or the lack thereof) that drives interest rate changes, not the other way around. Simply put, lower rates do not, in themselves, guarantee stronger growth. Now, this said…we do expect the government and fed to throw everything it can at juicing the economy. This might mean lower rates, among other liquidity inducing actions such as quantitative easing, bank de-regulation, accounting changes, etc.. So while the economy may be slowing it remains important to understand many levers exist that can lead to a large set of possible outcomes.

How We Got Here

We are still coming down from the stimulus-driven highs of the COVID era. While the process can be slow—sometimes feeling like “watching paint dry”—the aftereffects are now more visible. Flooding the economy with unproductive liquidity initially fueled rapid growth and inflation, but as that surge fades, it is leaving behind slower growth and the risk of stagflation.

Top-down efforts by governments to “juice” markets without corresponding productivity gains tend to create asset inflation rather than sustainable economic expansion. In other words, you can’t force the productive velocity of money without real production. Instead, excess liquidity often finds its way into asset purchases—pushing up home prices, gold, equities, and other assets—and exacerbating wealth inequality. This is, of course, a good reason to own equities and investments so that you might protect your spending power in these environments.

When money supply is increased without a matching rise in productive capacity, supply grows but demand does not. A clear visualization is giving your child the credit card. The supply of credit to buy things increased greatly for your child…but I doubt they will be using that credit to build a manufacturing plant and produce goods. The result in your house might be a lot of toys purchased on Amazon which is good for awhile but eventually the credit card will need paid. Without new income in the household that credit card in a child’s hands was simply not productive. In the real world, this behavior results in a distorted economy where asset valuations climb even as real economic growth struggles to keep pace. This imbalance is at the core of the stagflation risk we continue to monitor closely. Below are just a few data sources to support our view.

Question of the Quarter – Are Tariffs Inflationary?

I want to take a moment to answer some of the biggest client questions by tackling 1 major question a quarter. We hope you find value in this new approach to our regular updates:

Are Tariffs Inflationary?

The short answer: Yes… and No.

At its core, a tariff means a company must pay more to sell a product in the U.S. if that product isn’t made domestically. In theory, prices should rise by the effective tariff amount minus any portion the company chooses to absorb. When there’s little or no competition, businesses often pass most of the cost on to consumers. But in competitive markets, pricing becomes more complex, with companies adjusting carefully to protect long-term profitability.

As a result, some goods may become more expensive, while others see little to no price change. This suggests a short-term inflationary effect — but not necessarily a lasting one.

It’s important to remember that higher prices from tariffs reduce consumers’ spending power. If someone normally spends $1 on goods and one item rises from $0.70 to $0.77, they have only $0.23 left for other purchases instead of $0.30. That reduction in disposable income acts like a tax — and taxes tend to be deflationary over time because they pull money out of the economy rather than add to it.

This can sound counterintuitive, so let’s review:

- Inflation occurs when too much money is chasing too few goods.

- During COVID, government stimulus increased the money supply significantly while supply chain disruptions reduced available goods — a textbook recipe for inflation.

- Tariffs, in contrast, take money away from consumers without increasing the supply of goods, meaning less money is chasing the same amount of goods. Over time, that can slow economic activity and reduce inflationary pressure.

If tariffs are large enough, they could even have a deflationary impact. In practice, we may see a short-term bump in the Consumer Price Index (CPI) as higher costs work through the system, but the longer-term effect could become disinflationary — or, if demand slows significantly, even recessionary.

In short: Tariffs act like a “front-loaded” inflation hit followed by a potential drag on economic growth. Given all the nuance around how the full trade agreements will be instituted it becomes impossible to exactly know if we will have a long term net inflationary or deflationary pressure.

Final Thoughts

The market rebounded well in Q2 bringing us back to all time highs. We’ve already seen sharp shifts—from tariff-driven pessimism to renewed optimism around AI, trade agreements, and policy support. That wave of optimism, the anticipated rate cuts, the added liquidity has helped sustain today’s high water marks. But at current levels against a slowing economic backdrop and sticky inflation, the broader market is beginning to stretch our comfort zone.

We are continuing to take a balanced and cautionary stance. This could potentially mean giving up a few added percentage points of performance this year and in near future across all our management in a trade for focusing on protecting planning objectives long term. We will continue this subtle positioning of protecting against downside real risks while remaining open to upside surprises. We continue to lean in toward valuation discipline and diversification.

We continue to walk the line between optimism and realism. Elevated risks do not eliminate opportunity—but they do demand thoughtful, intentional positioning. Timing macroeconomic cycles is notoriously difficult, so our commitment remains to balance: making patient, prudent decisions grounded in long-term fundamentals.

Thank You

Let me again say—thank you. Our success is a shared result of great clients, great advisors, and a dedicated team. We’re incredibly grateful to wake up each day and do the work we love. It’s an honor to steward your hard-earned capital and walk with you toward your long-term goals.

Please reach out anytime with questions or thoughts.

Warmly,

Evergreen Wealth Management

Disclosures

- *Data reported by custodian Goldman Folio Institutional.

- *Data provided by YCharts reporting.

Index and ETF results (e.g., ACWI, AGG, S&P 500) do not reflect management fees or expenses and are not directly investable.

Evergreen Wealth Management, LLC is a registered investment adviser. This information is for educational purposes only and does not constitute an offer or solicitation to buy or sell any securities. Investments involve risk and are not guaranteed. Always consult with a qualified financial advisor or tax professional before implementing any strategy. Past performance does not guarantee future results.

The views expressed reflect the opinion of the firm as of the date indicated and are subject to change. Forward-looking statements are not guarantees and involve uncertainties that may cause actual results to differ.