March 9, 2026

/

To the Clients of Evergreen Wealth Management,

As we step into 2026, the team at Evergreen Wealth Management reflects on the privilege of guiding the financial futures of over 350 families and individuals. With more than $250 million in assets under management, we are deeply grateful for your continued trust and the meaningful relationships we’ve built—many of which span decades. Supporting your financial goals and retirement dreams is the heart of what we do, and it’s always top of mind for us.

In case you’re not keeping track of the amazing progress being made at Evergreen the past 10 years, we would like to communicate the high-level fast view milestones of what has taken place. I cannot emphasize enough how unique in our industry Evergreen has become. This is NOT normal! This progress is only possible because of Gods blessings, blessing to serve amazing families and supported by our amazing team of talented individuals.

2015 – Jeffrey and Michael Gorsline partner directly with portfolio manager Stephen Hanley to buildout a comprehensive vision of IN-HOUSE high-level planning and portfolio management for all clients. While everyone involved had worked extensively within the financial world for decades, we all shared a new vision on how clients could be served better.

2016 – Evergreen hires a research analyst (now a portfolio manager) Andrew Nutter to assist in trading, cash balance management, research analysis and compliance. We viewed the long-term vision in terms of decades and even a century not just years and looked to invest in a talented young person who could spend decades working directly with our lead manager through many market conditions before starting to steward assets for client accounts. Long term we aim to make sure client accounts have multiple managers and systems for checks and balances on thoughts and a backup manager(s) in place if needed.

2016 – Fourth Dimension Financial in Ohio joins up with Evergreen to utilize our money management services and offer a similar high-level in-house management to many of its clients. What a blessing they have been to our management team. They offer more than just clients but allow our Ohio offices to have a fun culture to share and challenge ideas freely, stress test business thoughts and express emotions which we think is very valuable as long-term investment managers. Sharpening thought skills daily is very important to management sustainability. The value of this relationship for our business goes deeper than just money management.

2016 – With the new relationship we officially launch our Perrysburg, OH office location with longer term vision that the money management team would be run out of Ohio and Planning/Operations would be housed in Williamston, MI.

2021 – We hire Kelsey Erickson as a full-time operations specialist to help all Evergreen operations move to the next level. As we continue to grow she continues to move into a Chief Operations Officer role and will eventually become the official COO of Evergreen. If you are going to get any single hire right…make sure its your operations head because they are the real magic and glue that holds all things service together! Kelsey is nothing short of an All Star and a big reason we have been able to offer and maintain high level service for the families we serve. We are beyond blessed to have her on the team.

2021 / 2022 – Evergreen purchases Haynes Financial adding roughly 50 additional households under our stewardship. As far as buyouts go, this was very smooth and allowed us to work with an amazing group of new families that we have blended perfectly into our Evergreen family. This is a big credit to John Haynes who helped steward these families prior to us and the value he added over many years allowed us to take over a good foundation and build upon it.

2025 – We hire associate advisor Cooper Gross to help increase our planning support, improve our planning software integrations and begin building into a full time Evergreen advisor. Cooper will grow into being our next great steward, supporting families and maintaining our expected high level of service.

Growing from $18 million of AUM to over $250 million in 10 years is not normal. However, growth has never been our benchmark. Accomplishing your desired long-term outcomes is our target. And while it is nice to reflect on what has happened….maintaining our culture, our service, our focus the next 10 years is what matter most.

We remain laser focused on providing you with a “high return on time.” We understand that your time is incredibly valuable, and our mission is to alleviate the burdens of financial management, so you can focus on what matters most to you. We aim to keep this letter high-level for your benefit, but if you have any deeper questions or would like more detail, please don’t hesitate to reach out!

2025 Market Reflections

2025 proved to be another great year in the markets.

Headlines throughout the year centered on artificial intelligence, geopolitical shifts, fiscal deficits, and interest rate policy. Yet when we step back and examine the drivers of equity returns over longer periods, corporate earnings growth remains the primary determinant of value creation. As we have shared each year and in many of our quarterly updates…the key to long term investing is owning a set of compounding profits and paying a fair price for that ownership.

Since this is the goal we must always evaluate fundamental success and progress in light of how profits are doing. Our key principle is that over long periods of time investment returns will reflect the earnings power of the underlying businesses IF you pay a fair price.

Here’s a snapshot of how key indices performed in 2025:

- All Country World Index (ACWI): +22.41%

- Dow Jones Industrial (^DJITR): +12.97%

- S&P 500 (SPY): +16.39%

- Aggregate Bond Index (AGG): +7.19%

*(1) Data above provided by Goldman Sachs Custody Solutions

While 2025 was a great year in both US Equity, World Equity and US Bond markets, the long term is what we aim our focus. Since the start of the decade (January 1, 2020), the ACWI has grown by 98.07%, which equates to an annualized return of 12.06%. This highlights the importance of staying focused on the long-term and avoiding knee-jerk reactions driven by short-term emotions.

Notably, during this same time we saw the aggregate bond market as reflected by AGG do very little and return only 5.36%; which is roughly 0.87% annual return rate. Inflation over the past 6 years within the US has been roughly 3.9%. This means your real return (net of inflation) if owning equities, depending on exact allocation would likely be around 8% gross of fees which is an exceptional real return. Owning or overweighting toward traditional US Treasuries on the other hand would have resulted in very subpar returns. Owning the aggregate bond index alone would have netted a loss of purchasing power of around -3% average each year or around -20% total loss of purchasing power since 2020.

This is why we warned against overweighting traditional bond portfolios as rates hovered near historical lows in 202/2021. Unfortunately, many seniors, pensions and mismanaged endowment funds made the mistake of this overweight and have not kept up with inflation leading to a decline in real wealth status. Similarly, those who do not have the luxury of investing have taken an extreme step backwards in wealth status as inflation has greatly reduced (taxed) the ‘non-investors’ within our society. This has resulted in what is labeled the K-shaped economy. Inflation spikes are the biggest issue for expanding the wealth gap and we saw pandemic stimulus induce this reality with full force from 2020 to 2024 to create todays K shaped economic reality.

K-Shaped Economy and K-Shaped Market

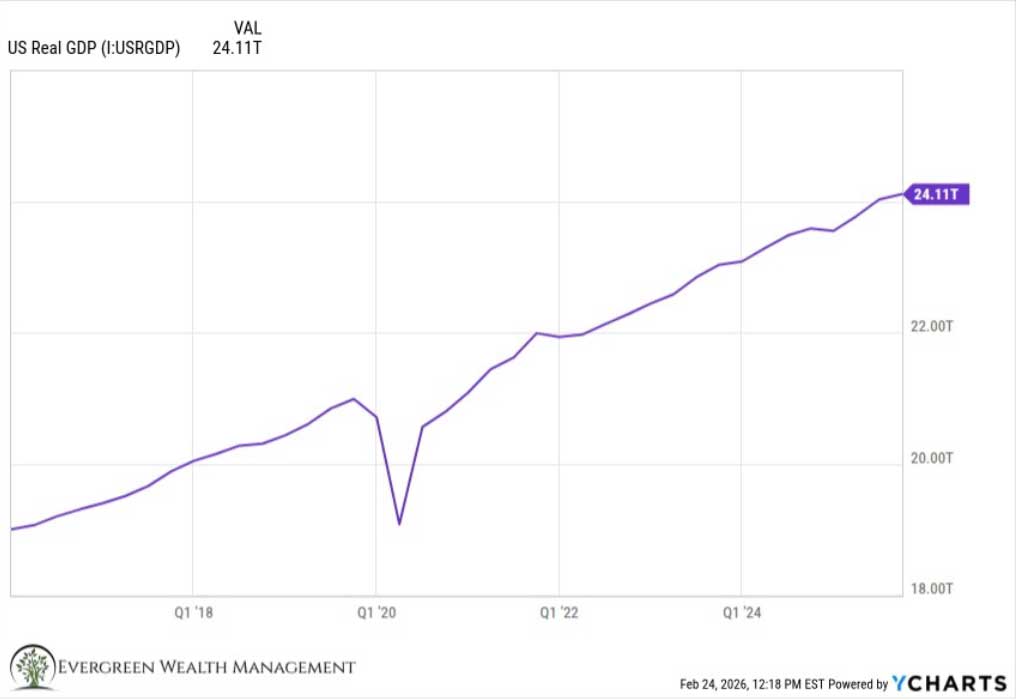

Overall the economy continues to march forward in very solid fashion with a 2.2% real (net of inflation) GDP growth for the USA in 2025 (*Data from Y-Charts). Continuing a solid march forward likely to continue in 2026.

However, under the surface you have a continuation of the post covid bifurcation highlighted by the larger wealth gap and the haves and have nots. As of Q3 2025, the top 1 % of households held ~31.7 % of total U.S. net worth, up from ~22–23 % in 1989 with a large portion of the gap explosion happening post covid as inflation expanded the trend. To put this in perspective the bottom 50% wage earners in Ohio is roughly 70K annual total household income while the top 1% is around $500K. Michigan is also fairly similar to these levels. So if you have a duel income family making near 500K you are close to the top 1%. Most investors are much closer to top 1% than the 50%!

This recent reality is not limited to just individuals but extended deeply into corporate America as well. Capital did not flow evenly. Instead, liquidity, stimulus, and passive index flows disproportionately have favored the largest, most profitable, most liquid companies—particularly those levered to technology and artificial intelligence. Mega-cap balance sheets strengthened, margins expanded, and multiples re-rated higher, while many small- and mid-cap companies faced rising input costs, higher borrowing rates, and far less access to cheap capital.

*Let me pause to emphasize a very key investing point everyone can understand. Given the choice between 2 identical products with 2 different prices…which one do you buy? The cheaper one correct! The low cost producer will win. Understanding who has access to cheapest capital is the same concept…the cheap capital in investing is key to producing the highest return on capital in most cases. The past 10 years have been dominated by the largest companies having almost monopoly like powers on accessing cheap capital. We will return to this thought later as we discuss AI and the new era we are entering that will shape market dynamics.

The result of this has been a corporate K-shape: companies with pricing power, scale, and data advantages accelerating forward, while more cyclical, capital-intensive, or rate-sensitive businesses lagged meaningfully behind.

In many ways this divergence was amplified by stimulus and ultra-low interest rates. But for most projects (outside of buying a house or real estate in general) those low rates are only accessible for big companies. I asked the bank to borrow money to build a data center and they laughed at my face…why? It was a great idea, in huge demand, I am willing to put down 20-30% and I couldn’t get the low rates a major hyperscaler company can get. I am only half joking because we did have conversations of other ideas and banks are unwilling to take any real risk for non-fed collateral ideas. This means the only players in town with access to all that cheap capital are the big boys and large private equity players…and they had very little competition and a lot of low and almost free capital!

When capital is free, duration expands and the market pays a premium for perceived certainty and long-term growth. AI enthusiasm further intensified this dynamic. Investors crowded into a narrow group of companies positioned as beneficiaries of the AI buildout—chips, hyperscalers, infrastructure providers—while capital-starved areas of the market saw multiple compression despite often improving underlying fundamentals. Liquidity begets liquidity, and index construction reinforced the concentration as market-cap weighted benchmarks pushed more dollars toward the same names.

However, for this expansion to remain durable and healthy, money cannot remain concentrated indefinitely. Sustainable economic growth requires breadth. AI-driven productivity gains must begin to diffuse beyond the infrastructure layer and into the broader economy—into industrials, healthcare, financials, manufacturing, small businesses, and regional enterprises. If AI remains primarily a capital expenditure cycle for a handful of mega-cap firms without translating into widespread margin expansion and earnings growth across the broader market, the divergence risks becoming structurally unstable.

Historically, strong bull markets that endure are characterized by participation. As financing conditions normalize and rates stabilize, smaller companies with solid balance sheets and improving return profiles should begin to benefit from broader credit availability and productivity enhancements. If AI truly represents a step-change in efficiency, its impact should eventually lower costs, expand margins, and enhance competitiveness across a much wider set of businesses—not just those building the data centers. When that broadening occurs, capital flows will likely follow, valuations will normalize across size segments, and the “K” begins to compress back toward a more balanced slope.

We believe the next sustainable phase of this cycle requires exactly that transition—from concentration to diffusion, from infrastructure spend to productivity realization, and from narrow leadership to broad participation. That shift would not only strengthen market durability, but also reduce the structural imbalances that have defined this decade so far. As optimist we hope this happens both in markets during the next 5 years AND in wages for the everyday Americans! If this happens everyone from major corporations to small business to employees will be a winner. New industries will be created and technology can fuel the next great wealth effect for all. But this is not without real risks along the way.

The AI Risk – Demand Destruction

One of the key risks if AI-driven growth does not diffuse more broadly is that the current capital cycle begins to resemble prior episodes of overinvestment. Today’s largest technology companies are deploying unprecedented levels of capital, and while earnings appear strong on a P/E basis, free cash flow tells a more tempered story as depreciation and stock-based compensation absorb much of the benefit. It now requires significantly more capital to generate each incremental dollar of revenue than it did a decade ago. If the return on this massive wave of investment comes in below expectations, margins and returns on invested capital could compress, particularly as size itself becomes a constraint on reinvestment efficiency. History has repeatedly shown that when capital intensity rises faster than sustainable end demand, mean reversion eventually follows.

The deeper concern lies not with infrastructure demand from hyperscalers (Amazon, Microsoft, Google, Meta), but with end-user adoption several layers downstream. AI infrastructure companies are currently experiencing extraordinary order flow, but ultimate justification depends on whether enterprises—and ultimately consumers—generate incremental revenue sufficient to earn an attractive return on that capital. Efficiency gains alone are unlikely to justify hundreds of billions in annual capex. Productivity improvements often translate into lower prices through competition, not permanently higher margins. If broad-based revenue growth does not materialize fast enough, today’s shortages in chips, power, and data center capacity could turn into tomorrow’s gluts, as has occurred in industries from telecom to energy to housing.

Shortages attract capital. Capital eliminates shortages. And when too much capital arrives at once, oversupply follows. The risk is not that AI lacks long-term value—it almost certainly will reshape industries—but that the timing and magnitude of investment overshoot the pace of real economic absorption. If diffusion into small caps, traditional industries, and the broader economy lags, the imbalance could result in a digestion period for mega-cap technology and a more painful correction for the infrastructure layer feeding the boom. For this cycle to remain sustainable, AI must transition from a concentrated capital expenditure story into a widespread productivity and earnings story across the full economic spectrum.

The Investment Conundrum

This dynamic brings us to a major investing question for the remainder of this decade. If AI adoption accelerates and the extraordinary capital expenditures by hyperscalers (Google, Amazon, Meta, Microsoft) ultimately generate attractive returns, today’s market concentration may prove justified. Broad indices, heavily weighted toward these beneficiaries, would likely continue to perform well as productivity gains translate into durable earnings growth. In that scenario, maintaining exposure to the dominant platforms could remain a rational and rewarding strategy.

However, if productivity gains arrive more slowly than anticipated—or if returns on the enormous capital deployed fall short—the implications are very different. A decline in return on invested capital at the largest companies would not only pressure their valuations, but also ripple through the ecosystem of suppliers, infrastructure providers, and service firms dependent on continued AI expansion. It would have far reaching impacts on our economy, banks and credit system. Given the current concentration within major indices, portfolios heavily reliant on passive exposure could face a prolonged period of muted or negative real returns, even if the underlying businesses remain fundamentally strong. Wonderful companies are not immune to cyclical capital digestion when excess investment meets slower-than-expected demand.

This places asset allocation at the forefront of prudent decision-making. Turning a blind eye to these risks may be rewarded if the optimistic scenario unfolds, but ignoring concentration risk has rarely been a durable strategy. Diversifying away from U.S. mega-cap exposure appears intuitive, yet it introduces its own complexities—potentially increasing sensitivity to other macro forces such as commodity inflation, currency volatility, or structurally slower-growth economies. There are no easy answers. We believe the path forward requires balance: maintaining exposure to innovation and quality businesses, while thoughtfully broadening participation across sectors, sizes, and geographies. In an environment where both landmines and opportunities are abundant—and where data remains early and often conflicting—discipline and flexibility will matter more than conviction alone.

While these macro discussions are important, what ultimately matters is how they affect your retirement income, your charitable goals, and your family’s future.

The simple answer is this…diversify, hold appropriate amount of lower risk assets to weather volatility, align allocation with your personal plans risk, income, tax and return needs and be opportunistic. We are doing all of this on a custom basis. For many of you that’s all you want to know; but for those who want a more detailed view keep reading.

Evergreen Wealth Response – Keep It Simple

Periods of structural change require clarity, not complexity. AI innovation, political transitions, shifting regulatory frameworks, and evolving geopolitical alliances are all reshaping the global economic landscape. The pace of change feels accelerated, and beneath the surface we are witnessing meaningful capital reallocations and market dislocations. This is not all bad, and in fact we are getting excited about certain areas of the market. But it does require a long-term view and prudent management to navigate.

Questions naturally arise: What happens if mega-cap technology companies moderate spending? How might Federal Reserve balance sheet policy influence liquidity? Could data center buildouts distort energy and material markets? Will AI disrupt entire layers of the software industry? How will geopolitics, regulatory and new capital alignments change markets? These are massively important questions that we are wrestling and analyzing as we position portfolios.

While we cannot forecast each outcome with precision, we can observe a broader pattern that has repeated throughout history. Transformational technologies (like the internet revolution) tend to democratize access over time. Just as the internet lowered the cost of distribution, research, and communication—empowering smaller firms to compete with entrenched incumbents (just think about how Evergreen has same tools as massive financial firms)—we believe AI will increasingly lower the cost of productivity tools, data analysis, and automation. This will allow new firms to compete well with larger incumbents and break down some competitive barriers.

Today, mega-cap firms are investing enormous capital to build the infrastructure for this coming change (which is why we will continue to own and have good exposure to the foundation makers). Over time, that infrastructure may become the foundation upon which smaller and mid-sized companies build competitive advantages of their own. If this diffusion occurs, some of tomorrow’s great compounders will likely emerge from areas of the market currently overlooked.

In response, we are generally broadening participation within portfolios by increasing exposure to small- and mid-cap equities through diversified ETF allocations and/or direct stock participation dependent on your specific plan needs. We are aiming to capture the potential beneficiaries and/or avoid some risks of technological diffusion while also reducing concentration risk. As always, we are modestly trimming certain direct equity exposures to manage new risks and reallocating toward high-conviction businesses that we believe possess durable balance sheets, strong free cash flow characteristics, and the ability to navigate multiple economic environments. Ultimately continuing to move toward balance alongside the capital balance and new opportunities we see unfolding in markets.

Along the same theme, we are looking to strategically increase international equity exposure as value allows. Global markets often move in multi-year cycles of leadership. As capital broadens and interest rate differentials evolve, international companies may benefit from lower valuations, currency shifts, trade realignments, and commodity dynamics.

Through all of these adjustments, our guiding principle remains unchanged: your plan comes first. We are not managing to beat a benchmark for a single year. We are managing to protect and grow real purchasing power over 5-, 10-, and 20-year horizons. That requires discipline, humility, and data-driven positioning—not bold predictions. In times of sea change, keeping it simple is often the most sophisticated strategy of all.

Closing Thoughts

Every decade presents its defining narrative. The 2010s were shaped by ultra-low rates and the dominance of scale. The early 2020s were defined by stimulus, inflation, and extraordinary market concentration. The remainder of this decade will likely be defined by how innovation—particularly artificial intelligence—moves from promise to productivity, from infrastructure buildout to real economic benefit.

We do not pretend to know the precise timing of how this unfolds. What we do know is that capital cycles always rebalance, innovation always diffuses, and disciplined investors who remain focused on earnings power, valuation, and risk management are ultimately rewarded. Our responsibility is not to chase headlines or avoid volatility altogether. Our responsibility is to steward your capital with prudence, humility, and conviction—positioning portfolios to participate in opportunity while guarding against permanent impairment of purchasing power.

As we enter 2026, we remain optimistic—not because risks are absent, but because opportunity is abundant. Markets may shift, leadership may rotate, and narratives will change. What does not change is our commitment to your long-term plan. We will continue to think independently, act deliberately, and keep your financial future at the center of every decision we make.

Thank you for allowing us to walk this stewardship journey with you. Serving you remains our greatest professional privilege.

With sincere gratitude,

Evergreen Wealth Management

Disclosures

(1) Data provided by custodian Goldman Folio Institutional.

(2) Data provided by Y-Charts.

Index results such as the All-Country World Index (ACWI), Dow Jones Industrial & S&P 500 do not reflect management fees and expenses, and you cannot typically invest in an index. Evergreen Wealth Management, LLC is a registered investment adviser. The information presented is for educational purposes only and does not constitute an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future results.

The opinions expressed herein are those of the firm and are subject to change without notice.